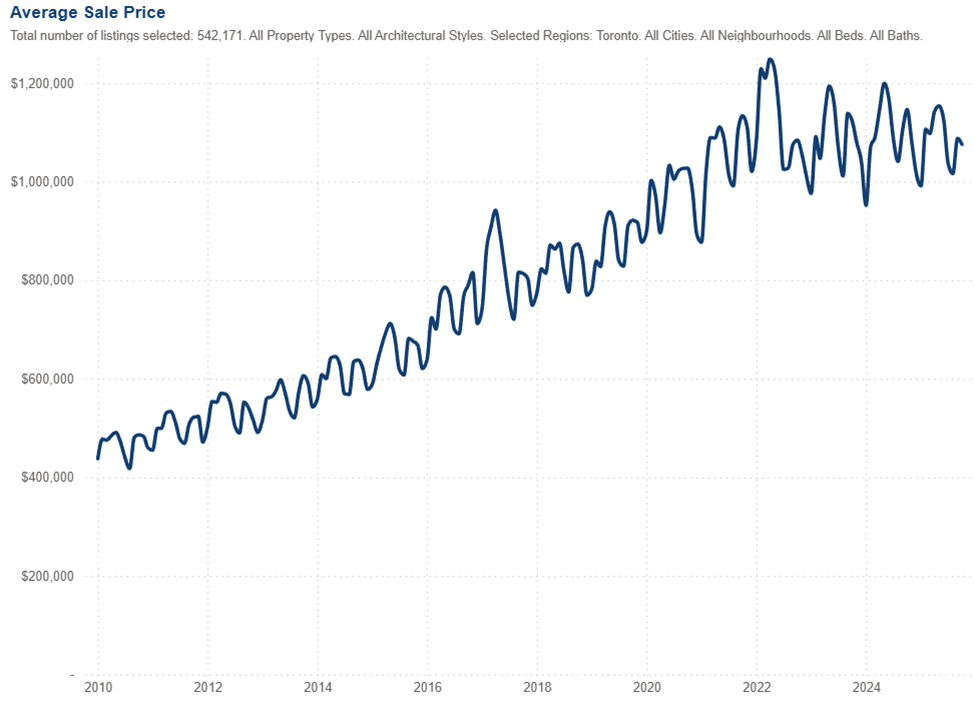

The typical homeownership journey for many buyers starts with a condo or townhouse and requires time and effort to build up equity in order to move up into a semi or detached property. This is not everyone’s journey, but it’s been a very common path especially for couples looking to start a family. And if you look at the average prices in Toronto over the last couple decades, it’s easy to see why this strategy was so popular.

Real Estate Prices historically rise over time with population and infrastructure growth and getting into the market sooner rather than later is a good strategy to ensure you’re not priced out over the long run.

Did you know we have a podcast? Listen to The Last Honest Realtor on our website or anywhere else you get your podcasts for the latest industry commentary and market insights.

But like all markets, there are ebbs and flows in the short term, and within the last couple of years we’ve seen some price depreciation in our market. This can be a great time to move up the property ladder or jump in as a first time buyer, as you’ll have much more leverage and can realize great value on purchase, but it’s important to understand how much equity (if any) you have in your current property before making any major decisions moves.

For some buyers, who may have purchased at the very top of the market, you may have little or even negative equity within your current property which will limit what and where you can go in the short term.

Do you have more questions about buying or selling real estate in Toronto? Here are a few more posts you might find useful next:

- What is the Worst Time to Sell a House?

- Can You Sell a Condo with a Special Assessment?

- Things that Fail a Home Inspection

Understanding Equity in Real Estate

When you hear real-estate professionals talk about equity, they’re usually referring to the difference between what your home is worth and what you still owe on your mortgage. Ideally, that number is positive: your home value exceeds your loan balance. But sometimes, especially in shifting markets or after buying with a small down payment, the opposite can happen. This is known as negative equity.

Negative equity—often called being “underwater” or “upside down” on your mortgage—occurs when the current market value of your home is less than the amount you owe the lender.

For Example; If you owe $450,000 on your mortgage but your home is currently valued at $400,000, you have –$50,000 of equity.

Negative equity can occur for several reasons:

- Market downturns: Rapid drops in home values can wipe out equity, especially if you bought during a peak.

- Low down payments: If you purchased with minimal money down, you start with little equity cushion.

- High-interest or unconventional loans: Interest-only loans or loans with adjustable rates can impede principal reduction.

- Declining neighborhood conditions: Local changes—new developments, zoning shifts, or increasing supply—can reduce values.

Having negative equity doesn’t automatically spell financial trouble, but it does limit your flexibility:

- You likely will not be able to sell without owing money to your lender.

- Refinancing becomes difficult unless you use specialized programs.

- Moving, upgrading, or downsizing can feel financially restrictive.

- If you face job changes or financial hardship or even experience a life change of another sort options for moving are narrow.

If you’re thinking of selling with negative equity there will be challenges to overcome, but you do have options.

1. Bring Cash to Closing – The simplest—but not always easy—option is to pay the difference between the sale price and mortgage balance.

- Pros: Clean break; no credit impact.

- Cons: Requires liquid funds.

2. Rent Out the Property – If selling isn’t viable, renting the home might cover your mortgage until market conditions improve.

- Pros: Buys time; potential for future price recovery.

- Cons: Landlord responsibilities; income might not fully cover expenses.

3. Wait It Out – Real estate markets are cyclical. If you can stay put, you may regain equity as you pay down the mortgage and market values rise.

- Pros: No credit impact; often the most financially sensible approach.

- Cons: Not an option if you need to move now.

Navigating negative equity is less about rules and more about strategy based on your situation. Consider:

- How quickly you need to move

- Your financial stability

- Your long-term housing plans

- Local market trends

- Your tolerance for renting or managing two properties

Most importantly and as always, regardless of the market cycle or your personally situation, it’s crucial to find and work with qualified real estate agent, financial advisor, and mortgage professional who can provide personalized guidance based on your local market and lending environment to

The right team around you is key to understanding your options, running the numbers, and maximizing the results of the route that aligns with your specific financial and lifestyle goals.

Looking for home-selling advice? Get in touch by filling out the form on this page, calling us at 416.642.2660 or emailing us at admin@torontorealtygroup.com.

Ready to Get Started?

It all starts with a conversation. Whether buying or selling, TRG can help you achieve your real estate goals. Get in touch with our team today to start the process.